Skip to content

Skip to content

TL;DR:

- Moving insurance specifically covers belongings during transport and handling by movers.

- Standard home or tenant policies often exclude fragile items, scratches, dents, and high-value goods during a move.

- Choosing the right coverage involves inventorying valuables, asking insurers detailed questions, and considering third-party policies for high-value items.

Most Ontario homeowners and renters assume their existing insurance policy will protect their belongings when moving day arrives. That assumption feels reasonable until a dresser gets scratched, a television screen cracks in transit, or an antique gets damaged and a claim is denied. Moving puts your possessions in a uniquely vulnerable position: they are being physically handled, loaded, transported, and unloaded by people and equipment outside your control. Understanding what moving insurance is, how it differs from your regular policy, and what your actual options are in Ontario could save you from a very costly surprise.

Table of Contents

- What is moving insurance and how does it work?

- What does your home or tenant insurance cover during a move?

- Types of moving insurance and coverage options in Ontario

- How to evaluate your risks and protect your valuables

- A moving pro’s perspective: what most people miss about insurance for their big move

- Get full peace of mind for your Ontario move

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Moving insurance is separate | Home and tenant insurance usually does not fully protect your belongings during a move. |

| Coverage gaps can be costly | Scratches, dents, and breakages are often excluded unless you add dedicated moving coverage. |

| Assess and ask | Inventory your valuables and talk to both your insurer and moving company before your move. |

| Choose coverage wisely | Opt for the right level of moving insurance based on your goods’ value and risk tolerance. |

What is moving insurance and how does it work?

With the groundwork set, let us clarify what moving insurance really is and clear up why it is different from other forms of coverage.

Moving insurance is a form of protection that specifically covers your belongings during the process of a professional relocation. This includes the loading, transit, and unloading phases of your move. It is not a general insurance product. It is designed for the precise window of time when your possessions are most at risk.

This distinction matters because most people conflate moving insurance with standard home or tenant insurance. The two serve very different purposes. As YouSet explains, tenant insurance protects your belongings in your home, while moving insurance is specifically about coverage during transport and handling by movers. One protects you while your items sit in your living room; the other protects you while those same items are being carried down three flights of stairs and loaded into a truck.

You can read more about understanding moving insurance and what coverage professional movers typically offer in Ontario.

Here is what makes moving insurance different from your standard home policy:

- It applies during the active moving process, not just when items are in a fixed location

- It covers handling errors, transit accidents, and physical damage caused by movers

- It is tied to the specific move, not your property address

- It can be purchased separately from a third-party insurer or offered by the moving company itself

Moving insurance is not a luxury for people with expensive furniture. It is a practical safeguard for anyone who cannot afford to replace what they own without financial strain.

Many people do not realise how significant the gap is between what their tenant or homeowner policy covers and what actually happens during a move. Fragile items, antiques, electronics, and artwork are all in transit together, often stacked or wrapped in ways that are unfamiliar. Even a careful and experienced moving crew cannot eliminate every risk entirely. Moving insurance fills that gap by providing coverage specifically tailored to the moving environment.

Understanding this distinction early gives you the clarity to make informed decisions rather than discovering your coverage gaps after something goes wrong.

What does your home or tenant insurance cover during a move?

Now that you know how moving insurance functions, it is natural to wonder what your current home or tenant policy already covers when you move.

The short answer is: less than most people expect. Standard homeowner and tenant insurance policies do offer some protection for belongings in transit, but there are meaningful limitations that Ontario residents need to understand before they assume they are fully covered.

TD Insurance notes that homeowner policies offer coverage for a set timeframe and typically exclude certain types of damage such as fragile item breakage. The coverage window matters. Many policies extend protection for up to 45 consecutive days while your belongings are in transit within Canada. That sounds generous, but it does not mean every item is covered in every situation.

Here is a summary of what standard policies typically do and do not cover during a move:

| Coverage area | Typically included | Typically excluded |

|---|---|---|

| Fire and theft during transit | Yes | N/A |

| Accidental breakage of fragile items | Rarely | Usually excluded |

| Scratches and dents from handling | No | Yes |

| High-value jewellery without endorsement | No | Yes |

| Items in a storage unit | Limited | Often excluded |

| Antiques and art | Rarely without endorsement | Usually excluded |

Some items in your home require what insurers call an endorsement, which is an add-on to your base policy that provides extra coverage for a specific category of belongings. High-value items like jewellery, musical instruments, and original artwork are common candidates for endorsements. Without one, your base policy may only reimburse you for a fraction of the item’s actual worth.

Pro Tip: Call your insurer at least two weeks before your move and ask specifically which items are covered during transit, what the time limit is, and whether scratches and dents are included. Get the answers in writing.

Your pre-move checklist should include a dedicated step to review your insurance policy before packing begins. Many people skip this step and then have no recourse when a claim is denied.

Key limitations to keep in mind under most Ontario homeowner and tenant policies:

- Time limits apply, often 30 to 45 days in transit

- Fragile item breakage is commonly excluded unless it results from a listed peril like fire

- Scratches and dents are almost never covered under standard policies

- High-value items may need separate endorsements to be fully protected

- Storage unit coverage is often limited and may require its own rider

Understanding these gaps is not meant to alarm you. It is meant to give you the information you need to protect yourself appropriately before, not after, your move.

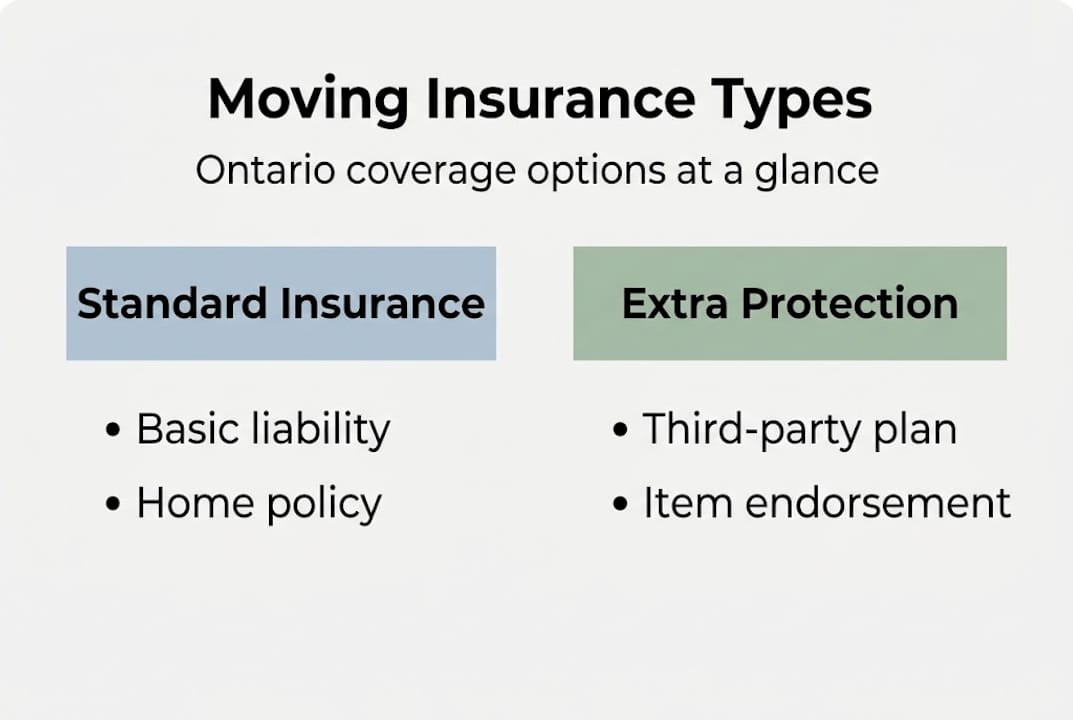

Types of moving insurance and coverage options in Ontario

With a clear sense of your home or tenant policy limits, you will want to know the insurance choices specifically tailored for moving. Here is how they compare.

There are three main types of moving-related coverage available to Ontario residents. Each comes with different levels of protection, different costs, and different situations where they make the most sense.

YouSet confirms that moving insurance coverage is focused on what happens during movement and handling by movers, which is exactly the gap your home policy often fails to address.

You can explore commercial moving insurance types in Ontario, or review insurance options with movers to understand what Aleks Moving offers its clients.

The three main types of moving coverage:

- Released value protection is the most basic option and is typically offered by moving companies at no additional charge. However, the trade-off is significant: coverage is calculated based on weight, not actual value. In Canada, this often amounts to a very small dollar amount per pound of goods. If your 10-pound flat-screen television is damaged, the payout may not cover even a fraction of its replacement cost.

- Declared value protection is a step up. You declare the total value of all your belongings, and the moving company accepts increased liability based on that declared amount. This option comes at an additional cost but provides much more meaningful coverage. If an item is lost or damaged, the mover is responsible for repair, replacement, or a cash settlement based on the declared value.

- Third-party moving insurance is purchased separately from a specialised insurer, completely independent of the moving company. This option is often the best choice for people with high-value items, fragile collectibles, or antiques that would not be fully covered under the first two options. Third-party policies can be tailored to specific items and offer broader protection.

| Coverage type | Cost | Coverage basis | Best for |

|---|---|---|---|

| Released value protection | Free | Weight per item | Low-value or everyday items |

| Declared value protection | Moderate added cost | Declared replacement value | Most standard household moves |

| Third-party moving insurance | Variable, can be higher | Item-specific or full value | Antiques, art, high-value goods |

How to choose the right coverage:

- List your most valuable items and estimate their replacement cost

- Check whether your home or tenant policy covers any of those items in transit

- Ask your moving company what they offer and what their claims process looks like

- Decide whether declared value or a third-party policy is more appropriate for your situation

- Get all coverage details confirmed in writing before your move date

The right coverage will depend entirely on what you own, what it is worth, and what you can afford to replace without financial stress.

How to evaluate your risks and protect your valuables

Understanding your options is only useful if you know how to actually protect what is most important. Here is a practical approach to evaluating your risks before moving.

The first step is to create a detailed inventory of your belongings before anything is packed. NACC recommends that you inventory your items and ask both your mover and your insurer about coverage during every stage of the move. This is not just good advice for insurance purposes. A thorough inventory helps you identify which items need special packing, which require endorsements, and which should perhaps be transported separately by you rather than by movers.

Start by walking through each room and documenting:

- Every item worth more than $200 by description, approximate value, and condition

- Fragile items that could be damaged by handling, including glassware, ceramics, and electronics

- Antiques or items with sentimental value that would be difficult or impossible to replace

- Items you already have endorsements or rider policies for under your existing insurance

Once you have your inventory, contact your insurer and your moving company separately. Ask each of them a very specific set of questions. Do not assume. Ask.

Pro Tip: Take timestamped photographs or a short video walkthrough of your belongings before packing day. If a claim arises, visual proof of condition is one of the most powerful tools you have.

TD Insurance confirms that coverage exclusions include short time windows, scratches and dents, and gaps for storage or transit periods outside the policy’s terms. Knowing these edge cases before you move means you can address them, not discover them later.

Knowing how to pack fragile items properly is also part of protecting your belongings. Some insurance policies include provisions that reduce coverage if items are not packed to a professional standard. This is especially relevant for long-distance Ontario moves where items spend more time in transit.

If your move involves specialty items like pianos, art, or antiques, review the special item moving tips available to Ontario residents. These items often require tailored protection well beyond basic coverage.

Also review your moving checklist to ensure that insurance review is built into your planning timeline, not left to the last minute.

Key questions to ask your mover before signing anything:

- What liability protection do you offer, and is it released value or declared value?

- What is your claims process if an item is damaged?

- Are there any items you will not accept liability for?

- Does your coverage apply during loading, transit, and unloading or only part of the process?

The answers will tell you exactly where the gaps are and what additional coverage you may need to arrange.

A moving pro’s perspective: what most people miss about insurance for their big move

After breaking down the practical steps, let us go behind the scenes with lessons experienced movers wish every customer knew.

The most common regret we hear from customers after a complicated claim is not “I wish I had more stuff covered.” It is “I wish I had read the fine print before I moved.” Most denied claims come down to three things: items that were fragile and excluded under the base policy, coverage windows that had already expired, or a lack of documentation proving the item’s condition before the move.

Here is something that surprises people: even when movers are professional and careful, liability is not the same as full replacement. Released value protection, which many people accept by default because it is free, is almost never enough to cover what something actually costs to replace. The gap between a policy payout and what your item is worth is a gap you pay for yourself.

Our strong advice, built from years of helping Ontario families relocate, is this: treat insurance review as part of your essential moving prep, not an afterthought. Document everything. Get coverage confirmations in writing. Ask questions early. Valuables that matter most to you deserve protection that matches their real worth, not the bare minimum someone else decided was sufficient.

Get full peace of mind for your Ontario move

If you want to avoid insurance stress and ensure your move goes smoothly, consider working with movers who care about your coverage as much as you do.

At Aleks Moving, we bring over 18 years of experience helping Ontario homeowners and renters relocate with confidence. We believe you deserve clear answers about your coverage, transparent pricing with no hidden fees, and a team that handles your belongings with genuine care. Whether you need trusted moving services for a local or long-distance Ontario relocation, or a combination of moving and storage service to suit your timeline, we are here to make the whole process straightforward. Reach out today for a free, upfront quote and let our family help move yours.

Frequently asked questions

Does my renters or homeowners insurance cover everything during my move?

No. Coverage in transit under homeowner or tenant insurance is time-limited and typically excludes breakage, scratches, and dents from handling.

Do I need moving insurance if professional movers are involved?

Yes, because professional movers provide basic liability, and most moving coverage by movers is limited in scope, making extra coverage essential for fragile or high-value items.

What kinds of damage are typically NOT covered under standard policies during a move?

Scratches, dents, and fragile item breakage are commonly excluded. Standard policy exclusions also often apply to antiques and high-value electronics during transit.

How do I decide how much moving insurance I need?

Inventory your belongings, identify your most valuable and breakable items, and then choose coverage that matches their actual replacement value. NACC advises that you ask your mover and insurer about every stage of the move before booking.

Is there a time limit for insurance to cover items while moving in Ontario?

Yes. Many policies extend transit coverage for 45 days within Canada, but this window and its conditions vary by insurer and policy type.