Skip to content

Skip to content

TL;DR:

- Moving valuation defines a moving company’s liability during transit but is not insurance. The default Released Value offers minimal coverage at no cost, while Full Value Protection provides more comprehensive coverage for a fee. Clients should carefully assess their shipment’s value, documentation, and potential gaps to choose the best protection option.

Moving valuation is the predetermined liability amount a moving company accepts for your shipment, setting the basis for compensation if items are lost or damaged during transit. This is not insurance. It is a federally mandated liability framework with two standard options: Released Value Protection and Full Value Protection. Every mover in Ontario planning a residential or commercial relocation needs to understand what is moving valuation before signing a bill of lading. The difference between these two options can mean the difference between a $30 payout and full replacement value on a $1,200 television.

What is moving valuation and how does it work?

Moving valuation is not insurance but a contractually defined level of carrier liability governed by federal standards. The moving company assumes financial responsibility for your belongings during handling, loading, transit, and unloading. You select your coverage level in writing on the bill of lading before the move begins. That document then governs any compensation if items are lost or damaged.

The two standard options are Released Value Protection and Full Value Protection. Released Value is the default option and costs nothing. Full Value Protection costs more but provides significantly better coverage. Understanding both is the foundation of managing your moving budget wisely.

What are the types of moving valuation protection?

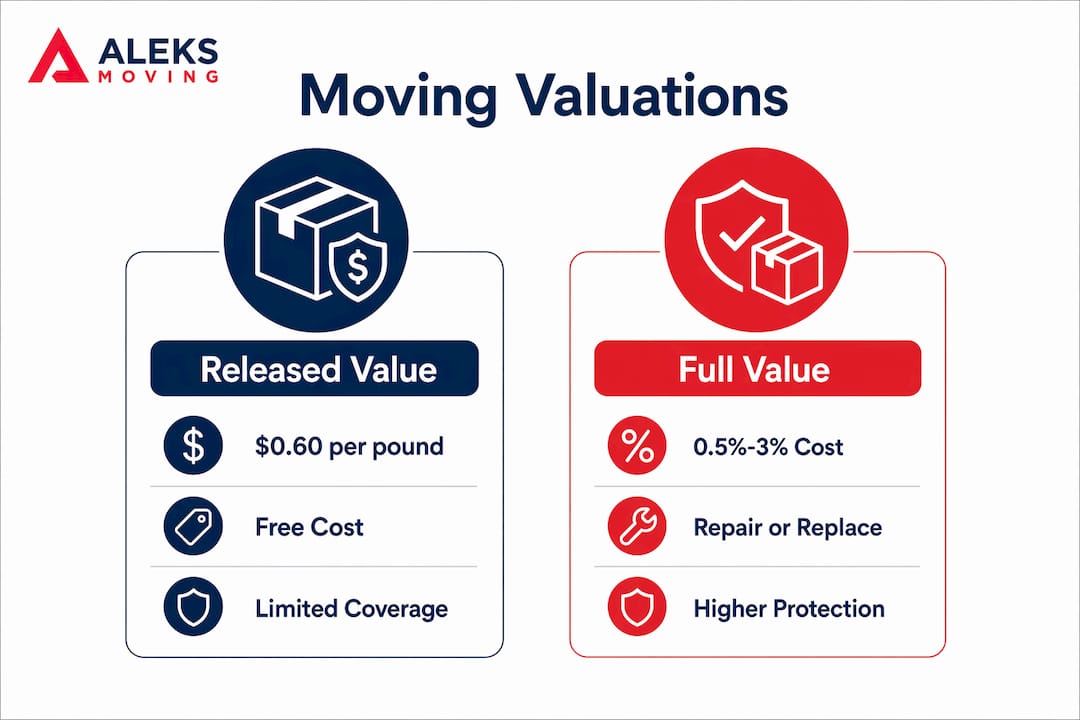

Released Value Protection

Released Value caps liability at $0.60 per pound per damaged article. That rate sounds straightforward until you apply it to real items. A 50-pound flat-screen television worth $1,200 would yield a payout of just $30. That gap between actual value and compensation is why this option, while free, carries serious financial risk for anyone moving electronics, antiques, or high-end furniture.

Full Value Protection

Full Value Protection requires the carrier to repair, replace, or pay cash equal to the replacement value of a damaged item. The remedy is the carrier’s choice under federal standards, with deductibles typically ranging from $250 to $500. This option costs roughly 0.5%–3% of your declared shipment value. On a $30,000 shipment, that means a premium between $150 and $900, depending on the carrier and deductible you select.

| Feature | Released Value Protection | Full Value Protection |

|---|---|---|

| Cost | Free | 0.5%–3% of declared value |

| Liability cap | $0.60 per pound per article | Full replacement value |

| Deductible | None | Typically $250–$500 |

| Best for | Low-value shipments | High-value or fragile goods |

Pro Tip: Always calculate the total replacement value of your shipment before choosing Released Value. If your goods are worth more than a few thousand dollars, the free option will almost certainly cost you more in the long run.

How does moving valuation differ from moving insurance?

Moving companies are not insurers and do not provide insurance products. Valuation is a limited liability framework under federal law. Insurance is a separate, state or provincially regulated product sold by licensed insurers. That distinction matters enormously when something goes wrong.

Valuation coverage has built-in exclusions that many clients do not expect:

- Self-packed boxes: Damage to owner-packed items is typically excluded unless there is visible external damage to the box.

- Acts of God: Floods, earthquakes, and similar events fall outside standard valuation coverage.

- High-value items: Jewellery, artwork, and collectibles often require separate declaration or are subject to lower liability caps.

- Mechanical or electrical failure: Internal damage to electronics without external evidence is frequently excluded.

Third-party moving insurance fills these gaps. A licensed insurer can cover perils that valuation contracts exclude, and the claims process runs through an independent party rather than the moving company itself. For anyone moving fragile or high-value items, third-party insurance is the more reliable safety net.

Pro Tip: Check whether your home or tenant insurance policy covers goods in transit. Some policies extend coverage during a move, which could reduce the cost of purchasing separate third-party insurance.

You can also compare moving insurance types to understand which combination of valuation and insurance best fits your specific move.

How to calculate moving valuation for your shipment

Calculating the right coverage level requires three steps: estimating your shipment’s total replacement value, understanding the carrier’s minimum declared value requirements, and selecting a deductible that balances cost and risk.

-

Create a detailed inventory. List every item you are moving with its current replacement value, not its purchase price or sentimental value. A detailed pre-move inventory is the single most reliable way to select accurate coverage and avoid disputes during a claim.

-

Apply the minimum declared value rule. Carriers often require a minimum declared value for Full Value Protection based on shipment weight, commonly set at $6 per pound. A 5,000-pound shipment would carry a minimum declared value of $30,000. If your actual replacement value is higher, declare the higher amount.

-

Calculate the Full Value Protection premium. Multiply your declared value by the carrier’s rate, which typically falls between 0.5% and 3%. On a $40,000 declared value at 1%, your premium is $400. Factor in your chosen deductible: a $500 deductible lowers the premium but means you absorb the first $500 of any claim.

-

Identify high-value items separately. Items worth more than a set threshold (often $100 per pound) may need to be listed individually on a high-value inventory form. Failing to do this can limit your compensation even under Full Value Protection.

-

Review and sign the bill of lading. Moving claims are governed by the bill of lading, which specifies all liability limits and remedies. Read it carefully before signing. Once the move begins, your coverage level is locked in.

| Declared value | Premium at 1% | Premium at 2% | Deductible |

|---|---|---|---|

| $10,000 | $100 | $200 | $250–$500 |

| $25,000 | $250 | $500 | $250–$500 |

| $50,000 | $500 | $1,000 | $250–$500 |

Understanding logistics payment structures can also help you budget for the full cost of your move, including valuation premiums and any processing fees.

What are the practical implications for Ontario customers?

Valuation coverage applies only while the moving company has direct control of your goods. That means coverage is active during loading, transit, and unloading. Once items are delivered and the movers leave, the liability period ends.

Several practical realities affect how claims play out:

- Self-packed boxes are a major risk. Valuation contracts exclude damage to owner-packed items without visible external damage to the container. If you pack your own boxes and something breaks inside, you will likely receive nothing under either valuation option.

- Deductibles reduce net payouts. A $500 deductible on a $600 claim means you receive $100. For smaller claims, the deductible can eliminate your recovery entirely.

- Documentation is your strongest asset. Photograph every item of value before the move. Note any pre-existing damage in writing on the bill of lading. This record is what supports your claim if damage occurs.

- File claims promptly. Most carriers require written notice of damage within a specific window after delivery. Missing that deadline can void your right to compensation.

Reviewing your asset protection options before moving day gives you a clear picture of what your carrier covers and where gaps exist.

Key takeaways

Moving valuation is a federally mandated liability framework, not insurance, and selecting the right option before your move is the most direct way to protect your belongings and manage financial risk.

| Point | Details |

|---|---|

| Valuation is not insurance | It is a carrier liability framework under federal law, not a regulated insurance product. |

| Released Value is risky | At $0.60 per pound per article, payouts rarely reflect actual item value. |

| Full Value Protection costs more | Expect to pay 0.5%–3% of declared shipment value, with deductibles of $250–$500. |

| Self-packed boxes are often excluded | Pack items yourself and you may lose coverage for internal damage without visible external harm. |

| Documentation protects your claim | Photograph belongings and note pre-existing damage on the bill of lading before moving day. |

Why most clients get this wrong, and what I tell them

People assume that because a moving company offers “valuation,” they are covered the way they would be with home insurance. That assumption causes real financial pain. I have spoken with clients who packed their own boxes to save money, chose Released Value to avoid the premium, and then received $18 for a broken $600 espresso machine. The math on that decision never works out.

The most common mistake is treating the free option as a reasonable default. Released Value Protection exists to give carriers a legal floor, not to protect you. If your shipment contains anything you could not replace out of pocket without stress, Full Value Protection is the correct choice.

The second mistake is skipping the inventory. A vague sense of what you own is not enough. Carriers require declared values, and without a written list, you have no baseline for a claim. Spend an hour before moving day photographing and listing your belongings. That hour is worth more than any premium you pay.

For high-value shipments, I always recommend pairing Full Value Protection with third-party insurance. Valuation has exclusions that insurance can fill. The combined cost is still a small fraction of what you stand to lose if something goes wrong without adequate coverage.

— Ali

Aleksmoving’s approach to valuation and your peace of mind

Aleksmoving has supported residential and commercial clients across Ontario for over 18 years, and transparent valuation guidance is part of every move we handle.

Our team walks you through both valuation options before you sign anything, so you understand exactly what coverage applies to your shipment. We follow federal valuation standards and help you select the declared value and protection level that fits your budget and the actual worth of your belongings. Whether you are planning a local move or a long-distance relocation, we make sure you are never left guessing about your coverage. Reach out to Aleksmoving to request a free quote and get clear answers about protecting your move from start to finish through our trusted moving services.

FAQ

What is moving valuation in simple terms?

Moving valuation is the level of financial liability a moving company accepts for your belongings during a move. It is not insurance but a federally mandated framework with two options: Released Value and Full Value Protection.

Is moving valuation the same as moving insurance?

No. Valuation is a carrier liability limit under federal law, while insurance is a separate product sold by licensed insurers. Insurance typically offers broader coverage and covers perils that valuation excludes.

How is Full Value Protection calculated?

Full Value Protection costs roughly 0.5%–3% of your declared shipment value, with a minimum declared value often set at $6 per pound of shipment weight. Deductibles typically range from $250 to $500.

What does Released Value Protection actually cover?

Released Value reimburses $0.60 per pound per damaged article. A 10-pound lamp worth $300 would yield a $6 payout. This option is free but provides minimal financial protection for most households.

When should I buy third-party moving insurance?

Purchase third-party insurance when your shipment includes high-value items, fragile goods, or self-packed boxes. Valuation coverage excludes many common damage scenarios that a licensed insurance policy can cover.